In recent Iowa speech, Perry echoes pre-recession, anti-regulation tone

DES MOINES — Texas Gov. Rick Perry swung through Des Moines on the caucus campaign trail last week, bringing a touch of Texas swagger to the Iowa Credit Union Convention while again railing against federal regulations

Jul 31, 20201.5K Shares752.6K Views

Image has not been found. URL: http://images.americanindependent.com/2012-80.jpgDES MOINES — Texas Gov. Rick Perryswung through Des Moines on the caucus campaign trail last week, bringing a touch of Texas swagger to the Iowa Credit Union Convention while again railing against federal regulations.

Perry, a candidate for the Republican presidential nomination, also jumped into an emerging disagreement over proposed legislation to ease lending limits that the federal government applies to credit unions. In return, these non-profit institutions don’t have to pay federal income taxes, which is a break their for-profit competitors – banks – don’t enjoy.

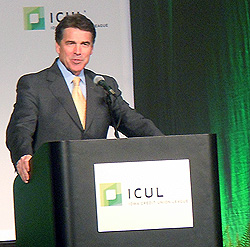

Gov. Rick Perry, candidate for the GOP presidential nomination, speaks at the Iowa Credit Union Convention in Des Moines, Sept. 16. (Photo: Emily Hoerner/IowaWatch)

During his 30-minute appearance at the convention, Perry focused on the legislation, the Small Business Lending Enhancement Act. It would raise the credit union member business lending cap from 12.25 percent of assets to 27.5 percent.

But some experts see parallels between the desire to loosen federal regulations, like credit union lending limits, and the anti-regulatory environment preceding the Great Recession.

Credit unions were created primarily to serve small savers and borrowers. Increasing the lending limit raises fears that credit unions are getting away from their mission and creeping into the market preserve of small community banks and larger commercial banks, both of which have to pay federal taxes.

By some estimates, the increase could create over 2,000 jobs in Iowa and help pump up an economy still feeling effects from the Great Recession, which started in late 2007. Potentially, raising the cap could dump more money into small business loans and into the economy.

Raising credit limits not a “no brainer”

“At first pass, it sounds like a no brainer,” said William C. Hunter, the dean and finance professor at the University of Iowa’s business college. But job and loan numbers are “just the tip of the iceberg.”

“Look at what happened to the housing market, Fannie and Freddie” Hunter said, referring to the housing market crash of 2007 and the two federally sponsored and supported mortgage financing institutions. “The laws grew more lax, the institutions drifted away from their original mission and the whole thing collapsed.”

While Hunter said he could not guarantee the same would happen if the lending cap were raised, he equated regulation change to a “slippery slope” that could lead to future repeals.

“If you go to 27, why not 50?” he asked. If legislators keep increasing the percentage, they need to take away the subsidies or private banks will be priced out of competition, he said.

The lending cap increase highlighted the anti-regulatory focus of Perry’s speech. The legislation boiled down to ending what he called the “nanny state” and taking a hatchet to federal regulations in an effort to create jobs and revenue.

“[If] you allow me to be the president of the United States, I will go to work every day to try to make Washington, D.C. , as inconsequential in your life as I can,” the governor said.

Perry takes aim at law to stop bailouts of out ‘too-big-to-fail’ companies.

The most direct reminder of the past regulatory laxity came sharply into focus when Perry also vowed to repeal the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. A major part of that law seeks to protect taxpayers from again having to finance huge bailouts of mismanaged financial institutions, which economists said had grown so big the economy could not afford their collapse.

In his critique of the 12-percent cap, Perry said the regulation was aimed at Wall Street but was damaging “Main Street” credit unions. This is not entirely true, because the cap is specifically directed at credit unions, which are, by definition, smaller institutions. According to the Credit Union National Association, banks hold nearly $13.4 trillion in assets, while credit unions hold a mere $885 billion.

When credit unions were created by the Federal Credit Union Act in 1934, they were intentionally limited.

“Credit unions were created for a certain niche, to create easy access to credit for small savers and borrowers,” said Hunter, the University of Iowa business college dean. “Today, credit unions have drifted away from that initial mission.”

But Perry praised this drift as a sign of economic growth. He said he planned to work closely with credit unions to limit regulations, hoping to create jobs by providing more loans to more people.

In Iowa, raising the cap could result in an additional 2,400 jobs and an influx of roughly $229,000, according data from the credit union association.

However, some financial experts, including Hunter, are wary of attaching such certainty to a change in regulation, primarily because of the impact it could have on private, commercial banks.

Because credit unions are non-profit organizations and tax exempt, they can offer loans at lower rates. It also means the federal government does not receive increased tax revenue from credit unions as they grow and lend more money.

Don Hole, the CEO and executive director of Community Bankers of Iowa, which represents for-profit small, independent bankers, opposed raising the cap. He cited revenue losses from waived income taxes, saying the lending cap would be an “unnecessary, additional burden on the taxpayer.”

But federal taxes are not the only way to oil economic wheels. Perry lauded the idea of giving loans to small businesses as a way of stimulating jobs.

In a stalled economy, small business loans are one of the few loans with an increasing demand. And studies show private banks are not granting many.

“Credit unions specialize in those smaller loans,” Perry said. “We need to consider alternatives, such as freeing up lending credit unions to help revive Main Street.”

Image has not been found. URL: http://media.iowaindependent.com/Iowa_Credit_Union_League_logo.jpgThe credit union association says credit unions have increased the number of small business loans by approximately 4.4 percent, while banks have increased by half that amount, 2.2 percent.

Looked at from another perspective, however, the numbers change.

According to figures from the Federal Reserve Bank of Chicago, credit unions loaned out $37 billion in small business loans in 2010. Community banks loaned out $300 billion and large banks loaned $270 billion.

Hole contended that community banks are willing to lend more, but the demand isn’t there. With the current economy, businesses are simply unwilling to borrow, he said. There is no evidence of eligible businesses being turned down.

A 2011 study by the New York Federal Reserve Bank supports Hole’s statement. It says businesses were hit harder by decreasing sales than denied loans.

Hunter cautioned against altering regulations until studies proved banks “rationed” loans.

“The market is an equilibrium. Changing it can mess things up,” he said, citing “the law of unintended consequences.”

Credit unions are intended to give small borrowers access to credit, Hunter said. Regulators should carefully examine any changes to make sure the institutions continue aiding this population instead of devoting too much capital to business loans and damaging community banks in the process.

“I like credit unions,” Hunter said. “They do give favorable rates to members. There’s nothing wrong with that as long as they don’t start doing what a bank does.”

Perry’s speech, unique in its focus on pending legislation, gives voters insight into his governing style: a limited government, invisible-hand-of-the-market approach. He promised to remove regulation from credit unions and other institutions.

One member of the audience, Eric Schurr of TMG Financial Services, said there was a “grain of truth” to the candidate’s statements.

“I think that the regulatory environment was too lax for a while,” Schurr said. “Now, the pendulum has swung too far in the other direction.”

But he cautioned against broadly excising all regulatory powers out the government.

“It is more important that a candidate have a realistic perspective of where the economy is, which is what will drive future solutions,” Schurr said.

This story was produced by IowaWatch.org, the non-profit, non-partisan news website of the Iowa Center for Public Affairs Journalism.

Camilo Wood

Reviewer

Camilo Wood has over two decades of experience as a writer and journalist, specializing in finance and economics. With a degree in Economics and a background in financial research and analysis, Camilo brings a wealth of knowledge and expertise to his writing.

Throughout his career, Camilo has contributed to numerous publications, covering a wide range of topics such as global economic trends, investment strategies, and market analysis. His articles are recognized for their insightful analysis and clear explanations, making complex financial concepts accessible to readers.

Camilo's experience includes working in roles related to financial reporting, analysis, and commentary, allowing him to provide readers with accurate and trustworthy information. His dedication to journalistic integrity and commitment to delivering high-quality content make him a trusted voice in the fields of finance and journalism.

Latest Articles

Popular Articles