Rent Vs. Buy Calculator - Making Informed Choices

Empower your housing decisions with the Rent vs. Buy Calculator. Financial insights for informed homeownership choices.

Author:Alberto ThompsonReviewer:Camilo WoodJan 25, 202412.5K Shares660.9K Views

The decision to rent or buy a home is a significant financial choice that influences your lifestyle and long-term financial goals. To aid in this decision-making process, individuals often turn to a powerful tool, the Rent vs. Buy Calculator. In this comprehensive guide, we delve into the intricacies of the Rent vs. Buy decision, exploring how the calculator works, the factors it considers, and how to interpret its results.

Understanding The Rent Vs. Buy Calculator:

The Rent vs. Buy Calculator is a financial tool designed to assist individuals in determining whether renting or buying a home makes more financial sense based on their unique circumstances. It takes into account various financial factors to provide a comparison of the overall costs associated with renting versus buying over a specified period.

Should You Buy Or Rent?

Think about your position before you decide whether to rent or buy. There are good times to buy and good times to rent. If you want to know if you're ready to become a homeowner, you should think about the pros and cons of both renting and buying. Find answers to the question "" and think about whether you want to own a house.

Example of an estimated monthly payment and APR: For a $464,000 loan with a 30-year term, an interest rate of 6.500%, a 25% down payment, and no discount points purchased, the monthly payment for the loan's principal and interest would be $2,933. The APR for the loan would be 6.667%.

Factors Considered By The Calculator

Home Price And Down Payment

The calculator considers the price of the home you are considering and the down payment you can afford. A higher down payment often leads to lower monthly mortgage payments.

Mortgage Terms

Mortgage terms, including interest rates and the length of the loan, are crucial factors. The calculator factors in the prevailing interest rates and the duration of the mortgage to calculate the total interest paid over the life of the loan.

Rent Costs

It accounts for your monthly rent costs, considering that renting typically involves fewer upfront costs but does not build equity.

Property Taxes And Home Insurance

Property taxes and home insurance are ongoing costs for homeowners. The calculator includes these expenses in the homeownership calculation.

Investment Return

For those considering investing their down payment instead of using it to purchase a home, the calculator factors in the potential investment return.

Home Appreciation

Home appreciation, or the increase in the value of the home over time, is considered. This is a crucial factor in determining the potential return on investment when buying.

Maintenance And Repair Costs

Owning a home comes with maintenance and repair responsibilities. The calculator incorporates an estimate of these costs over time.

How To Use The Rent Vs. Buy Calculator?

People don't usually ask and answer the question "Should I rent or buy?" just once. There are a lot of changing parts in this choice, and things can change: You save more for the down payment, you think about moving to a more or less expensive area, and you're interested in what happens if you spend more or less on a house.

That's all you need to use our Rent vs. Buy Calculator. These are seven facts that you may already know or have been thinking about:

- Where you wish to live.

- The price of the house (wondering how much house you can afford? You can use a Home Affordability Calculator to figure that out.

- The down payment you made.

- How long your mortgage is for (most people get a 30-year mortgage).

- How long do you plan to stay?

- How much it costs to rent a home like this.

To keep things simple, we guesses about some other common costs that are used in this estimate. You can see them, and it's easy to change the numbers to get a better result. You can see that we're assuming that your down payment is 20% and that your security deposit is 10% of the first month's rent. Again, though, you can change these numbers to fit your needs.

Interpreting Calculator Results

Break-Even Point

The calculator provides a break-even point - the number of years it would take for the costs of buying to equal the costs of renting. This is a key metric for decision-making.

Advantages Of Renting

If the calculator indicates that renting is more cost-effective, it may be advantageous for those seeking flexibility and avoiding the responsibilities of homeownership.

Advantages Of Buying

Conversely, if the calculator suggests buying is financially favorable, it signifies potential long-term benefits, such as building equity and potential home appreciation.

Sensitivity Analysis

Some calculators offer sensitivity analysis, allowing users to adjust variables like home price, interest rates, and investment return to understand how changes impact the decision.

Best Rent Vs. Buy Calculator

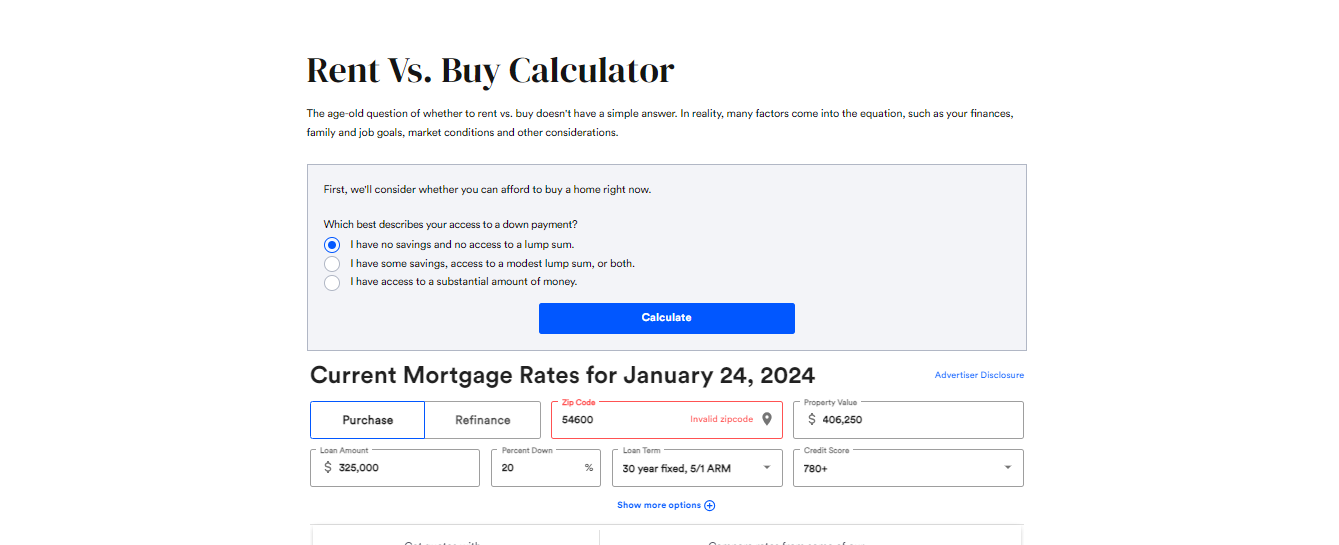

BankRate Rent Vs. Buy Calculator

The age-old question of whether to rent vs. buy doesn't have a simple answer. In reality, many factors come into the equation, such as your finances, family and job goals, market conditions and other considerations.

Visit their website to use this calculator.

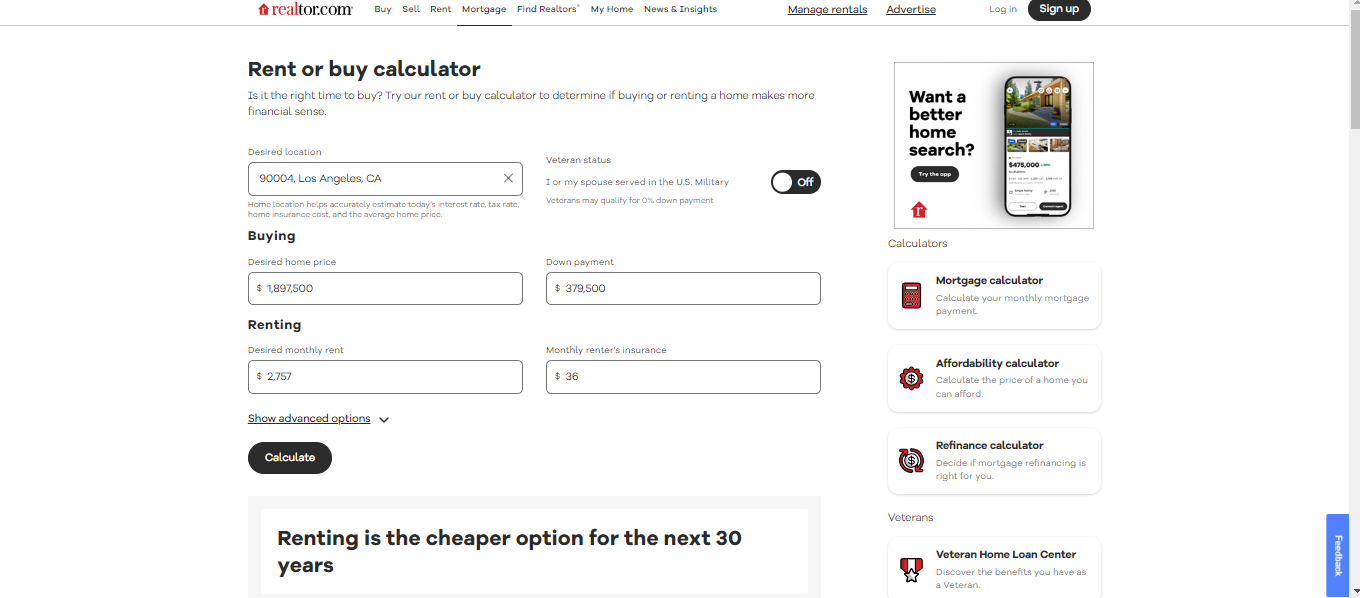

Realtor Rent Vs. Buy Calculator

Is now a good time to buy? Use this rent or buy toolto find out whether it makes more financial sense to buy or rent a home.

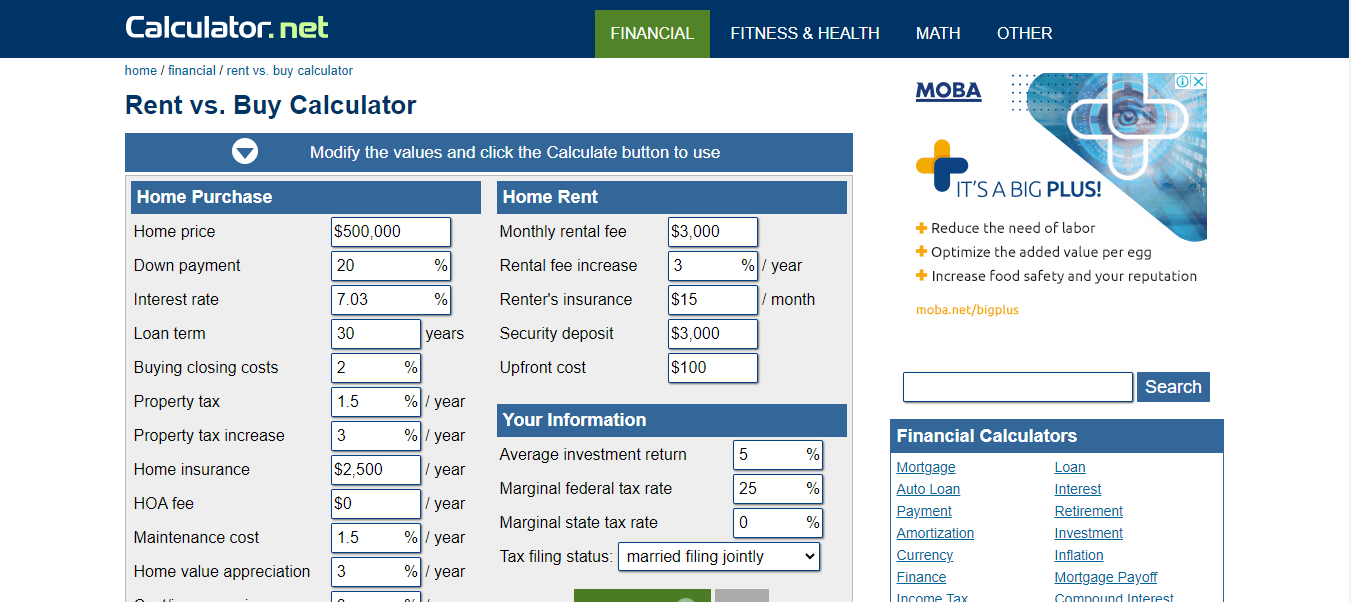

Calculator.net Rent Vs. Buy Calculator

Should I buy or rent? This is the most important question that every person who wants to buy a house will have to answer. This calculator can't exactly tell what will happen in the future, so the answer is only a guess based on the numbers you enter. Also, only people who live in the United States should use this tool.

When people really think about the Rent vs. Buy question, numbers can't show many of the intangible human factors that come into play. For example, the value of owning a home or not having to deal with renters is hard to measure.

Buyers sometimes want to be able to do things like paint their walls a certain color or have ten cats without their owners or neighbors complaining.

On the other hand, renters might rather have the security of knowing their monthly rent than having to pay a big down payment and closing costs all at once. People need to think about their own tastes when deciding whether to rent or buy.

Rent Vs. Buy Calculator - FAQs

How Does The Rent Vs. Buy Calculator Work?

The Rent vs. Buy Calculator evaluates the financial implications of renting versus buying a home by considering factors such as home price, down payment, mortgage terms, rent costs, and more.

What Factors Does The Rent Vs. Buy Calculator Take Into Account?

The calculator considers home price, down payment, mortgage terms, rent costs, property taxes, home insurance, investment return, home appreciation, and maintenance costs.

How Is The Break-even Point Calculated In The Rent Vs. Buy Decision?

The break-even point is the number of years it would take for the costs of buying to equal the costs of renting. It's a crucial metric provided by the calculator for decision-making.

What Are The Advantages Of Using A Rent Vs. Buy Calculator?

The calculator helps users assess the financial feasibility of renting versus buying, providing insights into potential long-term benefits, such as building equity and home appreciation.

How Does Home Appreciation Factor Into The Rent Vs. Buy Decision?

Home appreciation is considered as a potential return on investment when buying. The calculator assesses how the home's value may increase over time.

What Are The Limitations Of The Rent Vs. Buy Calculator?

While valuable, the calculator has limitations, such as not accounting for changes in personal circumstances or unforeseen market shifts. Users should complement the analysis with a holistic understanding of their unique situation.

Conclusion

The Rent vs. Buy Calculator serves as a valuable tool in the decision-making process, offering insights into the financial implications of renting versus buying a home. However, it's crucial to complement this analysis with a consideration of personal preferences, lifestyle, and long-term goals. By combining financial prudence with a holistic understanding of your needs, you can make an informed decision that aligns with your unique circumstances and aspirations.

Jump to

Understanding The Rent Vs. Buy Calculator:

Should You Buy Or Rent?

Factors Considered By The Calculator

How To Use The Rent Vs. Buy Calculator?

Interpreting Calculator Results

Best Rent Vs. Buy Calculator

Realtor Rent Vs. Buy Calculator

Calculator.net Rent Vs. Buy Calculator

Rent Vs. Buy Calculator - FAQs

Conclusion

Alberto Thompson

Author

Alberto Thompson is an acclaimed journalist, sports enthusiast, and economics aficionado renowned for his expertise and trustworthiness. Holding a Bachelor's degree in Journalism and Economics from Columbia University, Alberto brings over 15 years of media experience to his work, delivering insights that are both deep and accurate.

Outside of his professional pursuits, Alberto enjoys exploring the outdoors, indulging in sports, and immersing himself in literature. His dedication to providing informed perspectives and fostering meaningful discourse underscores his passion for journalism, sports, and economics. Alberto Thompson continues to make a significant impact in these fields, leaving an indelible mark through his commitment and expertise.

Camilo Wood

Reviewer

Camilo Wood has over two decades of experience as a writer and journalist, specializing in finance and economics. With a degree in Economics and a background in financial research and analysis, Camilo brings a wealth of knowledge and expertise to his writing.

Throughout his career, Camilo has contributed to numerous publications, covering a wide range of topics such as global economic trends, investment strategies, and market analysis. His articles are recognized for their insightful analysis and clear explanations, making complex financial concepts accessible to readers.

Camilo's experience includes working in roles related to financial reporting, analysis, and commentary, allowing him to provide readers with accurate and trustworthy information. His dedication to journalistic integrity and commitment to delivering high-quality content make him a trusted voice in the fields of finance and journalism.

Latest Articles

Popular Articles