The Pros And Cons Of Borrowing Money From Your Life Insurance Policy

Explore the pros and cons of borrowing money from your life insurance policy. Delve into the intricacies of policy loans, considering factors such as accessibility, tax implications, and impacts on cash value and death benefits. Make informed decisions with insights into the pros and cons of this financial option.

Author:Dexter CookeReviewer:Camilo WoodMar 03, 202422.5K Shares703.2K Views

If you need urgent cash, borrowing from your life insurance policy may be a tempting alternative, but before making such a choice, it's crucial to carefully considerthe pros and cons of borrowing money from your life insurance policy. This article examines the many facets of borrowing against your life insurance policy, covering everything from the fundamentals of life insurance to possible effects on the cash value and death benefit of your policy.

Comprehending Life Insurance Policies

It's important to have a firm grasp of how life insurance operates before discussing the benefits and drawbacks of borrowing from your policy. In a life insurance policy, you agree with an insurance provider whereby you pay premiums in return for a payout to your beneficiaries in the event of your death. Life insurance policies come in a variety of forms, including whole life and universal life insurance, as well as term and permanent life insurance. Every kind of policy has unique characteristics, advantages, and things to think about.

Summary Of Your Borrowing Choices

The cash value of the majority of permanent life insurance contracts is available for policyholders to borrow against. This kind of borrowing is frequently called a policy loan. Policy loans don't require collateral or a credit check, and their interest rates are usually lower than those of other loan kinds.

Furthermore, insurance loans are often exempt from taxes as long as the policy is active. To borrow against your policy, you must, however, be aware of the terms and circumstances, including the terms of repayment and any possible effects on the cash value and death benefit of your policy.

Pros Of Borrowing From Your Life Insurance Policy

A major benefit of taking out a loan against your life insurance policy is having the money available. Policies loans can be obtained quickly and easily, unlike traditional loans, which could need a drawn-out application process and credit check. Policy loans are a desirable choice for people in need of quick money because they often feature cheaper interest rates than other loan kinds. Moreover, policy loans don't have a predetermined payback schedule, giving borrowers financial flexibility.

Cons Of Borrowing From Your Life Insurance Policy

Even though taking out a loan against your life insurance policy can give you quick access to money, you should weigh the possible disadvantages. The possible effect on the death benefit and cash value of your policy is one major drawback. In essence, you are using your funds as collateral when you take out a loan against your policy.

Consequently, the cash value of your coverage is reduced by the amount borrowed plus interest. Furthermore, it may lessen the death benefit that will be given to your dependents if you cannot repay the loan. The value of your policy may also be further diminished by administrative fees and other costs connected to policy loans.

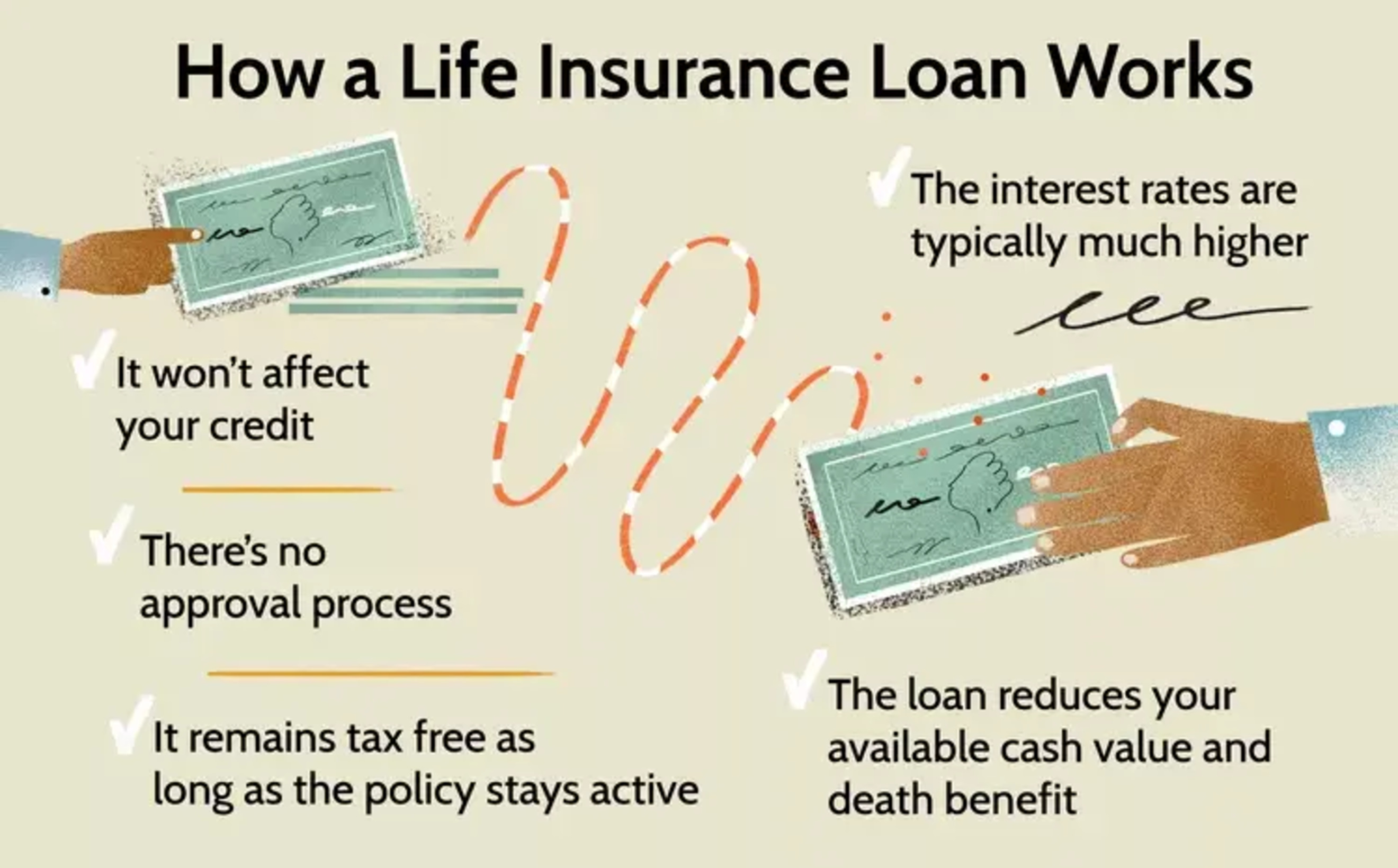

How A Life Insurance Loan Works

Since you are essentially borrowing from yourself, policy loans have no approval process or credit check, unlike bank or credit card loans, which have an impact on your credit. You can use the money you borrow against your policy for anything from bills to emergency savings to travel expenses—you are not required to explain how you intend to use it.

As long as the policy is in effect, the loan is likewise not taxable because the IRS does not consider it to be income (as long as it's not a modified endowment contract). A policy loan has no required monthly payment, but it is still expected to be repaid with interest (although the interest rates are usually much lower than on a bank loan or credit card).

Effect On Death Benefit

The possible effect on your policy's death benefit is one of the most important things to take into account when taking out a loan against your life insurance policy. When you take out a loan against your policy, the cash value of your policy is reduced by the loan amount plus interest. Repaying the loan may result in a reduction of the death benefit that will be paid to your beneficiaries after your passing. In addition, your insurance may lapse and you will no longer be covered if the outstanding loan total surpasses your policy's cash value.

Effect On The Cash Value

The cash value of your life insurance policy may be impacted by borrowing against it. The amount taken from the cash value of your policy is subtracted when you take out a policy loan. Furthermore, policy loans gradually accumulate interest, which lowers your insurance's cash worth even more. Your policy's cash worth could be completely depleted if you are unable to return the loan, leaving you with little to nothing left in it.

Considering Loan Repayment

When thinking about taking out a loan against your life insurance policy, it's critical to comprehend the conditions of repayment and your possibilities. Repayment terms for policy loans are usually flexible, enabling borrowers to repay the loan at their own pace. However, to prevent interest from accruing and possible effects on the cash value and death benefit of your policy, you must complete your loan repayments on time. Furthermore, if you are unable to repay the loan, the remaining amount due plus interest will be subtracted from the death benefit that will be given to your beneficiaries.

Tax Repercussions

A noteworthy benefit of taking out a loan against your life insurance policy is that policy loans are not subject to taxes. As long as the policy is in effect, policy loans are not taxable income, in contrast to other kinds of loans. Furthermore, policy loans are a tax-efficient borrowing choice because they do not result in capital gains taxes or penalties. To fully grasp the precise tax ramifications of taking out a loan against your life insurance policy, you need, however, to speak with a tax counselor or other financial expert based on your unique situation.

Alternatives To Borrowing From Your Life Insurance Policy

Even while taking out a loan against your life insurance policy can give you quick access to money, it's important to consider your options before choosing one. You might qualify for additional home equity loans, credit lines, or personal loans, based on your creditworthiness and financial status. To meet your financial needs, you can also think about selling off further assets or looking into other funding options. It's important to consider the advantages and disadvantages of each borrowing option and speak with a financial expert before choosing to take out a loan against your life insurance policy.

Frequently Asked Questions

Is It Bad To Borrow From Your Life Insurance?

Borrowing against life insurance can be a good option for those looking for a loan with low-interest rates, flexible repayment terms, and no credit check. However, it also comes with downsides like a reduced death benefit, risk of policy lapse, and significant interest accumulation.

What Is It Called When You Borrow Money From Your Life Insurance Policy?

Life insurance loans typically have lower interest rates than standard bank loans. A certain credit score is not required. Because you use the cash value in your policy as collateral on the loan, the insurance company does not need to check your credit score before approving the loan. CONS.

Can I Take Money Out Of My Life Insurance To Pay Off Debt?

Yes, it can be done. If you have the right type of life insurance – whole life or universal life – and have been making on-time payments to it for an extended period, you may have accrued enough “cash value” in the policy to bury your credit card debt.

Final Words

If you require urgent cash, borrowing against your life insurance coverage may be a good option. However, before making such a choice, it's crucial to thoroughly weigh the advantages and disadvantages. Policy loans have possible negative effects on your policy's cash value and death benefit in addition to accessibility, flexibility, and tax benefits. It's crucial to read the terms and circumstances of the loan, look into other borrowing choices, and speak with a financial expert before taking out a loan against your life insurance policy to make sure it fits with your overall financial goals and objectives.

Jump to

Comprehending Life Insurance Policies

Summary Of Your Borrowing Choices

Pros Of Borrowing From Your Life Insurance Policy

Cons Of Borrowing From Your Life Insurance Policy

How A Life Insurance Loan Works

Effect On Death Benefit

Effect On The Cash Value

Considering Loan Repayment

Tax Repercussions

Alternatives To Borrowing From Your Life Insurance Policy

Frequently Asked Questions

Final Words

Dexter Cooke

Author

Dexter Cooke is an economist, marketing strategist, and orthopedic surgeon with over 20 years of experience crafting compelling narratives that resonate worldwide.

He holds a Journalism degree from Columbia University, an Economics background from Yale University, and a medical degree with a postdoctoral fellowship in orthopedic medicine from the Medical University of South Carolina.

Dexter’s insights into media, economics, and marketing shine through his prolific contributions to respected publications and advisory roles for influential organizations.

As an orthopedic surgeon specializing in minimally invasive knee replacement surgery and laparoscopic procedures, Dexter prioritizes patient care above all.

Outside his professional pursuits, Dexter enjoys collecting vintage watches, studying ancient civilizations, learning about astronomy, and participating in charity runs.

Camilo Wood

Reviewer

Camilo Wood has over two decades of experience as a writer and journalist, specializing in finance and economics. With a degree in Economics and a background in financial research and analysis, Camilo brings a wealth of knowledge and expertise to his writing.

Throughout his career, Camilo has contributed to numerous publications, covering a wide range of topics such as global economic trends, investment strategies, and market analysis. His articles are recognized for their insightful analysis and clear explanations, making complex financial concepts accessible to readers.

Camilo's experience includes working in roles related to financial reporting, analysis, and commentary, allowing him to provide readers with accurate and trustworthy information. His dedication to journalistic integrity and commitment to delivering high-quality content make him a trusted voice in the fields of finance and journalism.

Latest Articles

Popular Articles