What Is A Fixed-rate Annuity? - Understanding The Basics

A fixed-rate annuity is a financial product where an individual invests a lump sum with an insurance company, receiving regular fixed payments over a predetermined period. The fixed rate ensures stable returns, making it a popular choice for risk-averse investors seeking steady income streams. What is a fixed rate annuity? Find out here.

Author:James PierceReviewer:Alberto ThompsonJul 17, 202469 Shares69.4K Views

When the question of what is a fixed-rate annuitypops up, what comes to mind? In the realm of financial planning and retirement management, fixed-rate annuities have emerged as a popular investment option. These unique insurance products offer a guaranteed interest rate for a specific period, providing individuals with a predictable income stream in retirement. In this comprehensive guide, we will delve into the details of fixed-rate annuities, exploring their key features, benefits, potential drawbacks, and the different types available in the market.

Defining Fixed-Rate Annuity

A fixed-rate annuity is an insurance product that establishes a contractual agreement between an individual and an insurance company. In this arrangement, the individual makes either a lump-sum payment or a series of payments. In return, they receive regular disbursements, beginning either immediately or at a future date. The primary characteristic that sets fixed-rate annuities apart is their guaranteed interest rate. This interest rate is determined at the time of purchase and remains constant for the specified period, providing stability and predictability for the annuitant.

How Does A Fixed-Rate Annuity Work?

A financial product that insurance companies offer is a fixed-rate annuity. Here's how it generally works:

- Initial Investment - When you purchase a fixed-rate annuity, you make an initial investment, either as a lump sum or through a series of payments.

- Guaranteed Interest Rate - The insurance company guarantees to pay you a fixed rate of interest on your investment for a specific period, which can range from one to ten years or more.

- Tax-Deferred Growth - The interest that your investment earns is tax-deferred, meaning you won't pay taxes on the interest until you start receiving payments.

- Payout Options - At the end of the accumulation period, you have several options for receiving payments. You can choose to receive a lump sum, a series of payments, or convert the annuity into a stream of income that can last for a set number of years or even the rest of your life.

- Security - The fixed-rate nature of the annuity provides a level of security, as you'll receive the agreed-upon interest rate regardless of market fluctuations.

- Death Benefit - Many fixed-rate annuities also offer a death benefit, which means that if you pass away before receiving payments, your beneficiary will receive the remaining value of the annuity.

It's important to note that fixed-rate annuities have some limitations, such as early withdrawal penalties and potential fees. As with any financial product, it's crucial to carefully consider your financial goals and consult with a financial advisor to determine if a fixed-rate annuity is the right choice for your circumstances.

What's The Difference Between A Deferred And Immediate Fixed-Rate Annuity?

A deferred fixed-rate annuity and an immediate fixed-rate annuity are both financial products offered by insurance companies, but they have different structures and payout schedules.

Deferred Fixed-Rate Annuity

- With a deferred fixed-rate annuity, you invest a lump sum or make periodic payments over time, and the annuity accumulates interest during an accumulation phase.

- The funds grow tax-deferred until you choose to start receiving payments, typically at a later retirement date.

- The payout phase begins at a future date of your choosing, and you receive regular payments for a specified period or the rest of your life.

Immediate Fixed-Rate Annuity

- An immediate fixed-rate annuity is purchased with a lump sum payment.

- The annuity starts providing a stream of income payments immediately or within a short period, generally within one year of purchase.

- The payments are typically fixed and guaranteed for the chosen payout period, which could be for a specific number of years or the rest of your life.

The key difference lies in when the payouts begin: deferred fixed-rate annuities start their payout phase at a future date, while immediate fixed-rate annuities begin providing income almost immediately after the initial investment. Both types of annuities provide a measure of financial security and can be a valuable part of retirement planning, but they serve different purposes depending on an individual's financial goals and circumstances.

What Are The Benefits Of Fixed-Rate Annuities?

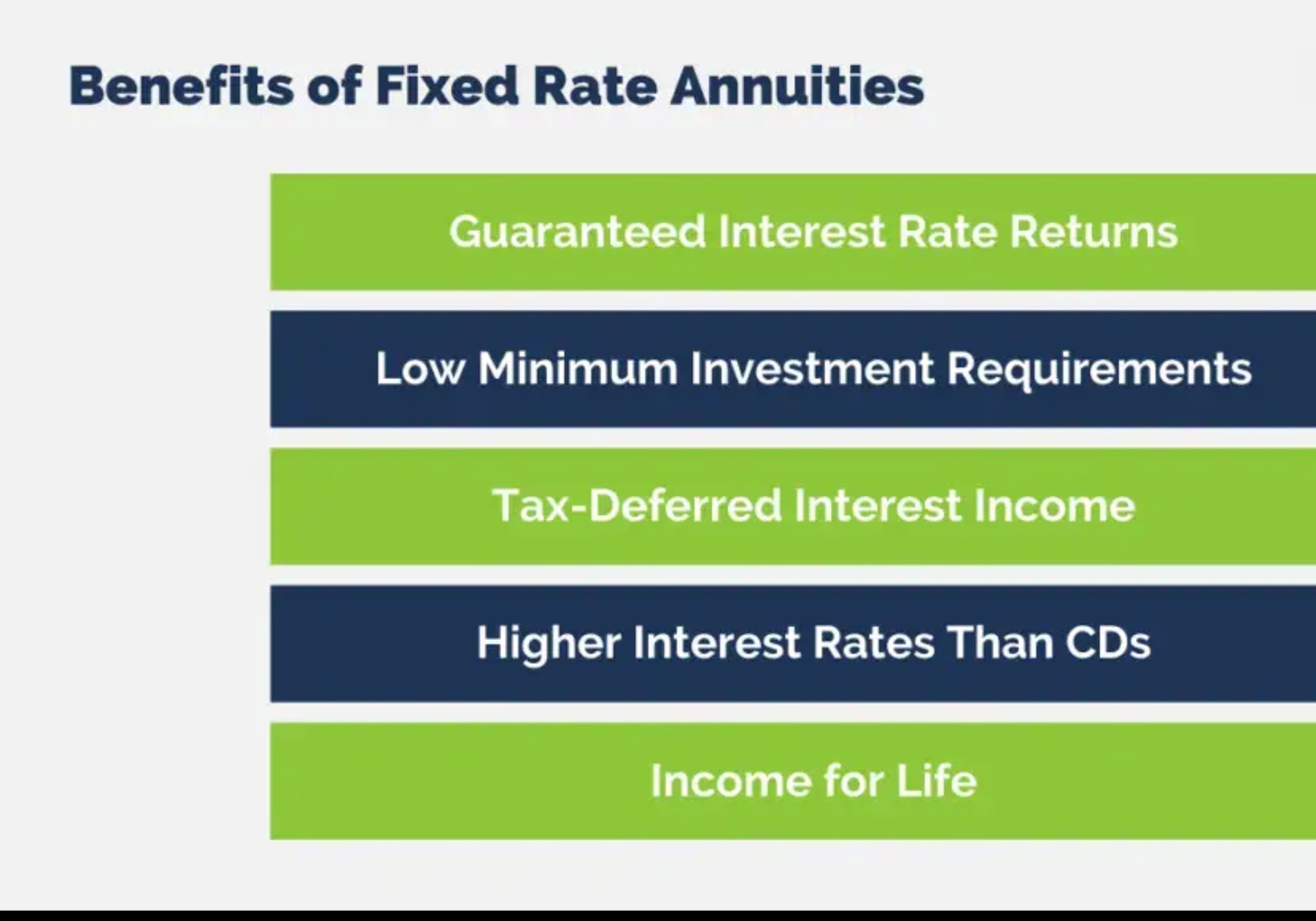

The benefits of investing in a fixed-rate annuity are compelling and contribute to their standing as a preferred investment vehicle for retirement planning. Some of the key benefits include:

- Guaranteed Returns - One of the most prominent advantages of fixed-rate annuities is the assurance of guaranteed returns. This provides annuitants with a sense of confidence in their long-term financial security.

- Tax-Deferred Growth- The tax-deferred nature of the annuity's growth during the accumulation phase allows investments to potentially grow more quickly, as taxes are postponed until the funds are withdrawn.

- Predictable Income Stream for Retirement - With competitive interest rates and flexibility in payout options, fixed-rate annuities offer a predictable income stream for retirement, allowing individuals to plan their finances with greater certainty.

- Protection of Principal and Interest - Fixed annuities offer protection for the premium and accumulated interest, thereby ensuring a stable foundation for the annuitant's financial future and safeguarding them from market volatility.

- Lower Investment Minimums and Beneficiary Protection- Fixed annuities typically have lower investment minimums compared to other financial products, making them accessible to a wide range of investors. Additionally, they provide beneficiary protection, ensuring that the designated beneficiaries receive the benefits in the event of the annuitant's passing.

What Are Some Downsides To Fixed-Rate Annuities?

While fixed-rate annuities offer a host of benefits, it's crucial to consider their potential drawbacks. Some of the key drawbacks include:

- Inflation Risk - Fixed-rate annuities may not keep pace with inflation, as the interest rate remains constant for the specified period. This could potentially diminish the purchasing power of the annuitant over time.

- Impact of Low-Interest Rate Environments - In environments marked by low-interest rates, fixed-rate annuities may yield lower returns compared to other investment options. This can pose a challenge in terms of generating substantial income from the annuity.

- Lack of Flexibility in Income Payments - Once the income payments are locked in at the time of purchase, there is limited flexibility to adjust them. This lack of flexibility may not align with the changing financial needs of the annuitant.

- Penalties for Early Withdrawal or Surrender - There may be penalties associated with early withdrawal or surrender of the annuity, restricting the annuitant's ability to access the funds in the annuity without incurring financial penalties.

What's The Difference Between A Fixed-rate Annuity And A Variable Annuity

Fixed-rate annuities and variable annuities are both types of annuities offered by insurance companies, but they differ significantly in how they operate and the risks they entail:

Fixed-Rate Annuity

- Guarantee- Fixed-rate annuities provide a guaranteed interest rate on the principal investment for a predetermined period. This means the annuitant receives a fixed amount of income during the payout phase, regardless of market fluctuations.

- Risk- The insurance company bears the investment risk in a fixed-rate annuity. Even if the underlying investments do not perform well, the annuitant's income remains unchanged.

- Stability - Fixed-rate annuities offer stability and predictability, making them suitable for individuals seeking a reliable source of income in retirement.

- Flexibility - Fixed-rate annuities typically offer fewer investment options and less flexibility compared to variable annuities.

Variable Annuity

- Investment Options- Variable annuities allow annuitants to invest their premiums in a variety of sub-accounts, similar to mutual funds. These sub-accounts are subject to market fluctuations and can include stocks, bonds, and money market instruments.

- Potential for Growth- Unlike fixed-rate annuities, the value of variable annuities can fluctuate based on the performance of the underlying investments. While this offers the potential for higher returns, it also exposes the annuitant to market risk.

- Flexibility- Variable annuities offer more flexibility in terms of investment choices and the potential for higher returns. However, this comes with greater volatility and uncertainty.

- Income- During the payout phase, the income received from a variable annuity is not fixed and can fluctuate based on the performance of the underlying investments. There is no guarantee of a minimum income amount.

The key difference between fixed-rate annuities and variable annuities lies in the level of risk and return. Fixed-rate annuities offer a guaranteed income stream with lower risk but limited growth potential, while variable annuities provide the opportunity for higher returns but come with greater market risk and volatility. Individuals should carefully consider their risk tolerance and investment objectives before choosing between the two options.

What's The Difference Between A Fixed-rate Annuity And An Indexed Annuity

Indexed Annuity

- Performance Tied to an Index- In an indexed annuity, the annuitant's returns are tied to the performance of a specific financial index, such as the S&P 500 or Dow Jones Industrial Average. The annuity's growth is based on the index's performance over a set period.

- Potential for Growth- Indexed annuities offer the potential for higher returns compared to fixed-rate annuities because they allow participation in market gains. However, the returns may be subject to caps, spreads, or participation rates set by the insurance company.

- Protection Against Losses- While indexed annuities offer the opportunity for growth, they also provide downside protection. The annuitant's principal is typically protected from market losses, ensuring a minimum level of return, even if the index performs poorly.

- Variability- Unlike fixed-rate annuities, the returns on indexed annuities can vary based on the performance of the underlying index. This means the annuitant's income during the payout phase may fluctuate, depending on market conditions.

The main difference between fixed-rate annuities and indexed annuities lies in how their returns are determined. Fixed-rate annuities offer a guaranteed interest rate, providing stability but limiting potential growth, while indexed annuities tie returns to the performance of a specific financial index, offering the potential for higher returns but with some level of market risk and variability. Individuals should carefully consider their risk tolerance and investment objectives when choosing between the two options.

Key Features Of Fixed-Rate Annuities

Fixed-rate annuities offer several key features that make them an attractive option for individuals seeking financial security and a reliable income stream in retirement. Some of the prominent features include:

- Guaranteed Interest Rate- Annuity providers set the fixed interest rate at which a fixed-rate annuity grows. This feature allows individuals to enjoy a predictable income stream, offering a sense of security and stability in an often unpredictable financial landscape.

- No Exposure to Market Performance - Unlike variable annuities, fixed annuities are not linked to stock market performance. Ensuring that the annuitant's investment is immune to market fluctuations, adds another layer of security against volatility.

- Predictable and Safe - These annuities are straightforward with guaranteed returns, making them a safe investment option. The predictability of the income stream and the assurance of receiving the promised returns add to their appeal.

- Tax-Deferred Growth - During the accumulation phase, the accumulated interest in the annuity grows tax-deferred, providing an opportunity for the investment to grow more efficiently over time.

- Options for Payout - An individual can choose immediate payments or defer payments to start at a later date based on their specific financial needs. Moreover, fixed annuities can be structured to provide income for life, offering a valuable tool for retirement income planning.

What Is A Fixed-rate Annuity? - FAQ's

What Defines The Term Fixed-Rate Annuity?

With a fixed annuity, you'll lock in an interest rate and receive guaranteed minimum payouts later in life, distributed in an amount that will be specified in your contract. If you have an immediate fixed annuity, you'll typically begin collecting payouts within a year after you sign the contract.

What Defines A Fixed-Term Annuity?

A fixed-term annuity is a retirement product that pays a guaranteed income for a set period. If you're looking for a guaranteed income but don't want to make a lifelong commitment with your pension savings, then a fixed-term annuity could be for you.

What Are The Rules Of A Fixed Annuity?

Every fixed annuity has a current interest rate and a minimum guaranteed interest rate. The company guarantees it will pay no less than a minimum rate of interest. During the payout period, the amount of each income payment to you is generally set when the payments start and will not change.

Final Words

In conclusion, fixed-rate annuities represent a valuable financial tool for retirement planning, offering a reliable and predictable income stream, guaranteed returns, and tax-deferred growth. While they have certain drawbacks, such as inflation risk and limited flexibility, their benefits outweigh the potential challenges for many investors. Understanding the key features, benefits, drawbacks, and the different types of fixed-rate annuities is essential for making informed investment decisions that align with one's financial goals and risk tolerance. As with any financial product, it is advisable to seek guidance from a qualified financial advisor to assess individual circumstances and explore the suitability of fixed-rate annuities as part of a comprehensive retirement strategy.

Jump to

Defining Fixed-Rate Annuity

How Does A Fixed-Rate Annuity Work?

What's The Difference Between A Deferred And Immediate Fixed-Rate Annuity?

What Are The Benefits Of Fixed-Rate Annuities?

What Are Some Downsides To Fixed-Rate Annuities?

What's The Difference Between A Fixed-rate Annuity And A Variable Annuity

What's The Difference Between A Fixed-rate Annuity And An Indexed Annuity

Key Features Of Fixed-Rate Annuities

What Is A Fixed-rate Annuity? - FAQ's

Final Words

James Pierce

Author

James Pierce, a Finance and Crypto expert, brings over 15 years of experience to his writing. With a Master's degree in Finance from Harvard University, James's insightful articles and research papers have earned him recognition in the industry.

His expertise spans financial markets and digital currencies, making him a trusted source for analysis and commentary. James seamlessly integrates his passion for travel into his work, providing readers with a unique perspective on global finance and the digital economy.

Outside of writing, James enjoys photography, hiking, and exploring local cuisines during his travels.

Alberto Thompson

Reviewer

Alberto Thompson is an acclaimed journalist, sports enthusiast, and economics aficionado renowned for his expertise and trustworthiness. Holding a Bachelor's degree in Journalism and Economics from Columbia University, Alberto brings over 15 years of media experience to his work, delivering insights that are both deep and accurate.

Outside of his professional pursuits, Alberto enjoys exploring the outdoors, indulging in sports, and immersing himself in literature. His dedication to providing informed perspectives and fostering meaningful discourse underscores his passion for journalism, sports, and economics. Alberto Thompson continues to make a significant impact in these fields, leaving an indelible mark through his commitment and expertise.

Latest Articles

Popular Articles